Maintaining uninterrupted financial velocity is the absolute core of any international online casino or sports betting traffic operation on Meta. In the high-stakes iGaming market, advertising campaigns live and die by their scale. When an optimization pixel locates an active, high-depositing user demographic within a Tier-1 country, the media buying team must immediately inject massive capital to maximize their return on investment.

However, moving substantial financial volume within gray-hat or policy-adjacent advertising setups frequently triggers immediate security protocols. The automated financial compliance scanners deployed by Meta’s core accounting network apply a hyper-sensitive risk grid to casino ad placements.

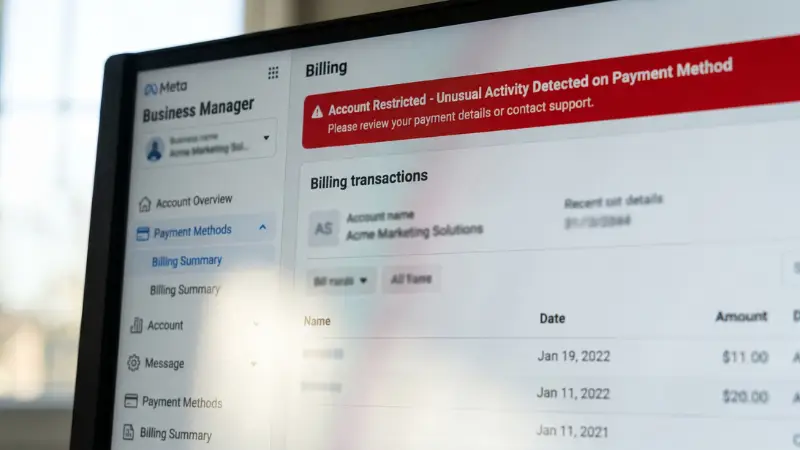

The primary operational blockers resulting from these automated scans are sudden, permanent payment method flags Meta ads system blocks and devastating automated security holds. This engineering report details the backend infrastructure reasons behind billing restrictions and outlines the precise architectural steps required to permanently fix unusual activity hold gambling errors to preserve your continuous cash flow.

The Anatomy of Financial Flagging: Why Meta Locks Casino Billing Pipelines

Meta’s backend accounting infrastructure relies on deep telemetry tracking to protect its advertising networks from transactional defaults and automated policy evasion. When a media buying team binds a new payment instrument or spikes their spending trajectory inside an iGaming ad funnel, the automated risk engine cross-references the connection signature across three specific structural parameters.

A. BIN Location and IP Routing Mismatches

Every credit, debit, or prepaid card possesses a Bank Identification Number (BIN)—the initial six to eight digits that define the specific issuing institution and country of origin. If a media buyer operates out of Southeast Asia using clean residential proxies located in the United Kingdom, but links a corporate billing card issued by a financial entity registered in an entirely separate region, the systemic misalignment triggers an immediate security warning. The automated scanners flag the session for card-identity deception, putting an immediate stop to active ad delivery.

B. Sudden Funding Velocity Anomalies

Traditional retail ad accounts naturally exhibit low spend momentum, slowly working their way up from small daily thresholds. Casino media buyers, however, operate under fast-paced market parameters. When an account shifts from spending $50 a day to attempting a multi-thousand-dollar funding scale within a single 12-hour cycle, the financial ledger’s internal risk monitors classify the sudden budget velocity as a major warning sign. The platform automatically pauses active campaigns to defend against potential fraud before human reviewers can audit the account logs.

C. Subnet and Transactional Risk Association

Meta maintains a massive historical database of corporate banking BINs used across its networks. If your team sources billing cards from a generic or public fintech application whose card pools have been heavily utilized by black-hat scrapers, bad actors, or non-paying ad teams, the entire underlying card pool becomes permanently flagged. Binding an instrument from a contaminated BIN pool results in systemic, automated account disables, completely bypassing any manual review of your actual ad creatives.

Advanced Mitigation Framework: Clean Corporate BIN Structuring

Resolving persistent billing flags requires moving past superficial card cycling strategies. High-volume marketing conglomerates minimize risk by building custom, localized corporate billing networks.

To establish deep billing trust, your internal financial division must isolate every operational cluster by sourcing private, premium corporate BIN lines that allow for localized geolocation matching. Ensure your cards match the exact geographic footprint of your active anti-detect browser and proxy nodes. If your operational assets route through United Kingdom residential subnets, your corporate funding cards must register native UK banking origins to clear automatic platform verification tests smoothly.

Step-by-Step Technical Restoration Protocol for Financial Holds

When an account encounters an automated restriction due to billing variations, executing the incorrect recovery sequence can result in a permanent structural ban on your Business Manager. Your operations division must enforce this strict technical restoration workflow:

Step 1: Immediate Connection Session Quarantine

Never attempt to immediately remove the flagged card or forcefully link a secondary card instance into the restricted profile. This behavior mimics programmatic automated scripts and locks the backend database permanently. Instantly pause the active anti-detect browser session and allow the connection footprint to cool for a minimum 6-hour window.

Step 2: Verification of Funding Authorization Settlement

Cross-reference your corporate banking log files to locate the temporary verification micro-charge issued by Meta (typically a random $1.00 USD authorization hold). Ensure the payment request was fully cleared and settled by your financial processor, rather than blocked by automated anti-fraud security filters at the banking level.

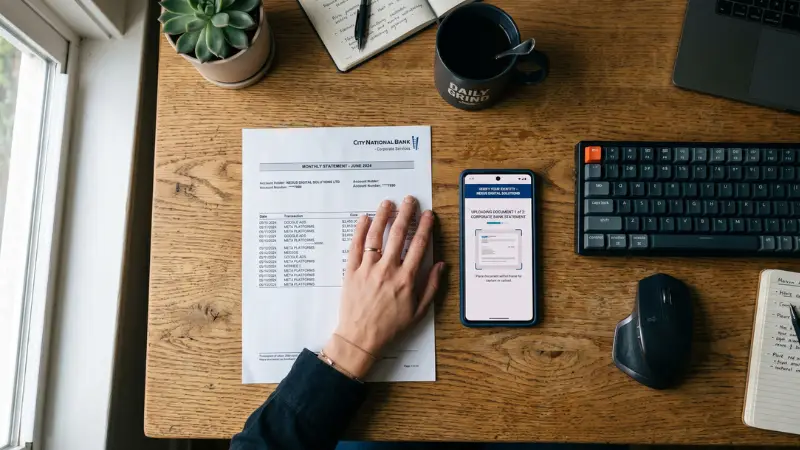

Step 3: Serving Sovereign Verification Artifacts

When executing the manual appeal protocol via the platform help tools, provide clear, unedited documentation showing real corporate presence. Upload high-resolution physical photographs of the corporate billing card resting on a clean office background surface, showing only the cardholder name and the last four digits, placed next to an official bank statement that verifies your company’s registered address. Providing this unedited physical evidence satisfies Google and Meta’s core trust algorithms, resulting in rapid manual clearance.

The Structural Apex: Moving Capital Allocation onto Authoritative Agency Lines

While implementing clean proxy nodes synchronized with premium private BIN instruments isolates your billing footprint from generic automated flags, running high-volume gambling funnels through retail business accounts remains an uphill battle. Standard business profiles are constantly exposed to unexpected spending chokes and manual review delays that interrupt your scaling momentum.

To establish complete financial continuity and eliminate the operational risk of administrative payment holds, growth enterprises abandon individual retail card attachments entirely. The definitive technical strategy involves migrating your media spend onto authoritative corporate partner accounts.

Deploying your casino campaigns through a premium Facebook casino ads agency account managed by established corporate compliance partners such as Optimal.to provides an unyielding layer of operational security:

- Pre-Vetted Institutional Credit Lines: Accounts provisioned by Optimal.to do not rely on fragile retail card binding configurations. These assets operate via pre-verified, centralized corporate line credit structures backed directly by legacy Meta Partner parent nodes. This pre-existing financial trust shields your assets from automated payment flags completely.

- Unrestricted Daily Spend Capacities: Eliminate the frustration of spend velocity freezes. Rented corporate agency logs allow your optimization lead to scale active daily budgets to $5,000, $20,000, or over $50,000+ smoothly from hour one, ensuring your campaigns capture peak consumer market volume without friction.

- 15-Minute Capital Allocation Protection: Working with an institutional traffic provider protects your operational balance sheet from sudden platform changes. If a macro platform update flags an active account node, the expert engineers at Optimal.to execute an immediate hot-swap protocol—safely recovering your deposited funds via backend API lines and transferring 100% of your balance to a fresh, active corporate log within 15 minutes, ensuring your funnels never stop running.

Frequently Asked Questions

Meta flags cards based on structural trust footprints, not just your available cash balance. If your card originates from a generic virtual fintech provider, shares a dải Subnet with fraudulent operations, or is linked from an IP address that doesn’t match the card’s issuing country, the automated systems will trigger a hold for security protection.

Absolutely not. Reusing a billing card that has been tied to a restricted asset creates a direct cross-contamination footprint. The system will permanently blacklist the card number, and attempting to bind it to a clean profile will cause an immediate, automatic account ban.